In our latest investor compass, we emphasized market euphoria, the rally in deeper detail, and the reasons for the rally - https://www.ambit.co/publication/199/Investor%20compass

We try to understand the dichotomy between the returns amongst the categories and try to identify what set of companies will lead the next leg of the rally.

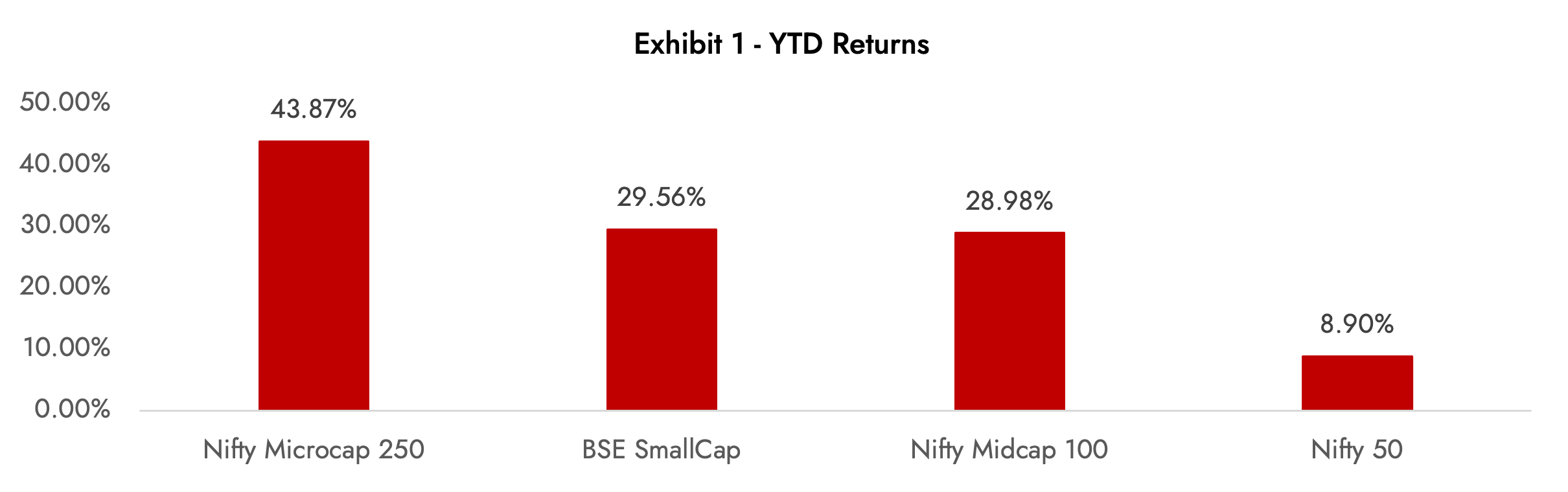

Exhibit 1 - YTD Returns

Source: Ambit Asset Management, Investing.com. YTD returns are till 27th September, 2023

VALUATIONS

Despite markets closer to all-time highs, valuations have materially moderated from all-time highs in a lot of large caps and high-quality mid and small caps. (Exhibit 2)

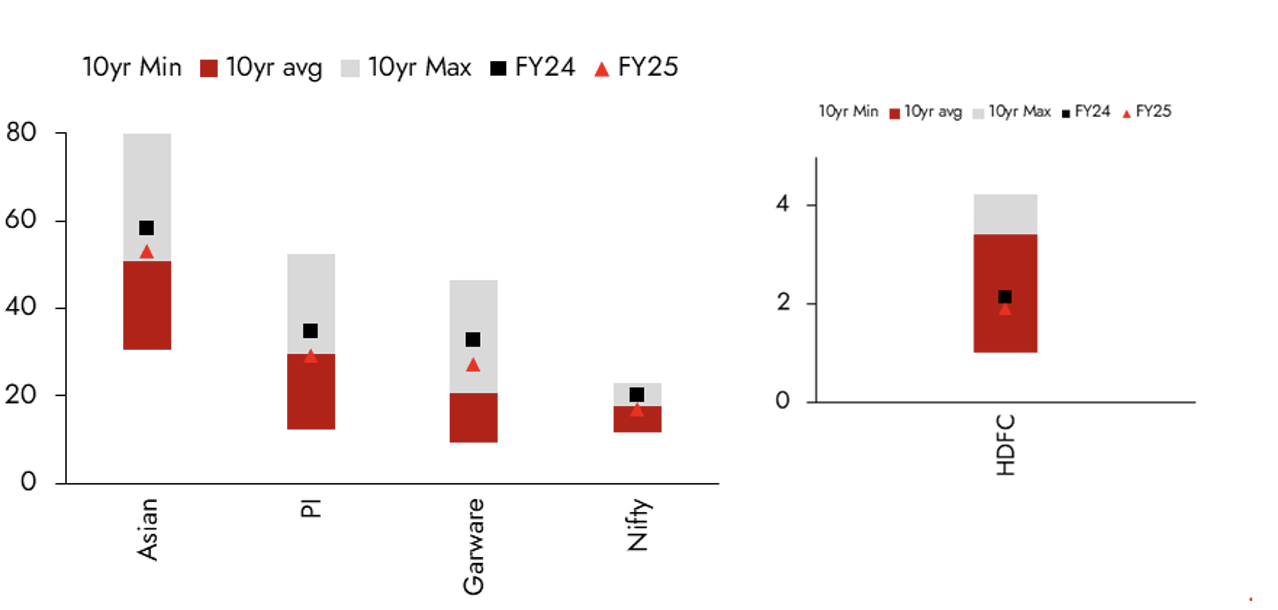

Exhibit 2 – Forward PE / PB multiples for Nifty 50 and Portfolio companies

Source: Ambit Asset Management, Bloomberg consensus

We analyse reasons for valuation moderation for some of our portfolio companies, key risks and fears for companies, and whether we anticipate them to bounce back strongly.

Asian Paints:

Asian Paints valuation has moderated materially (~85x PE to ~55x PE) owing to concerns over the sustainability of growth due to -

- Increase in competitive intensity in paints.

- Doubts over the ability to scale up adjacencies

COMPETETIVE INTENSITY

- Over the past 2 decades, MNCs and Indian companies have entered/ intensified - Sherwin Williams, Nippon Paints, Jotun Paints, Akzo Nobel, JSW, and Indigo Paints.

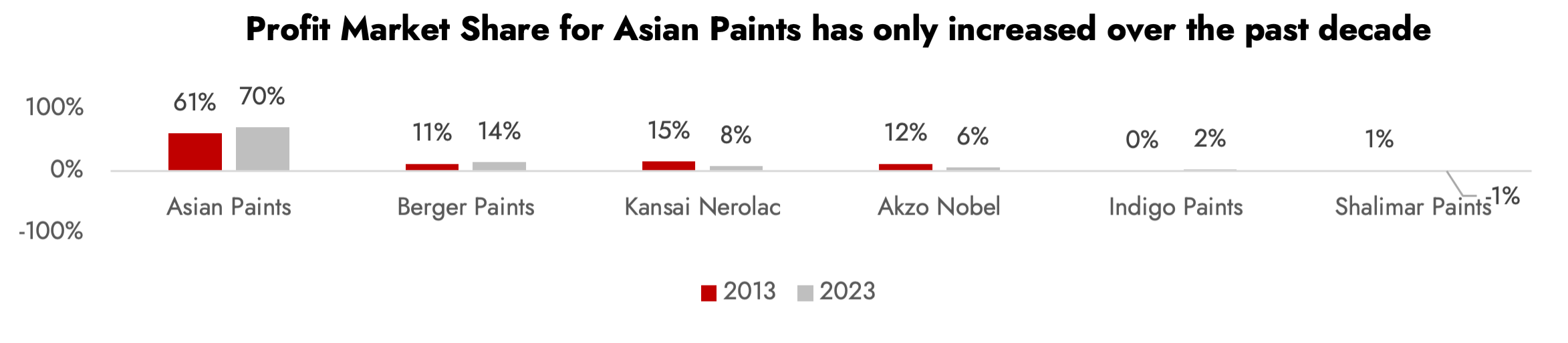

- Despite everything, Asian Paints market share has improved materially over the past decade and revenue and profit pool for newer entrants has been inconsequential. (Exhibit 3)

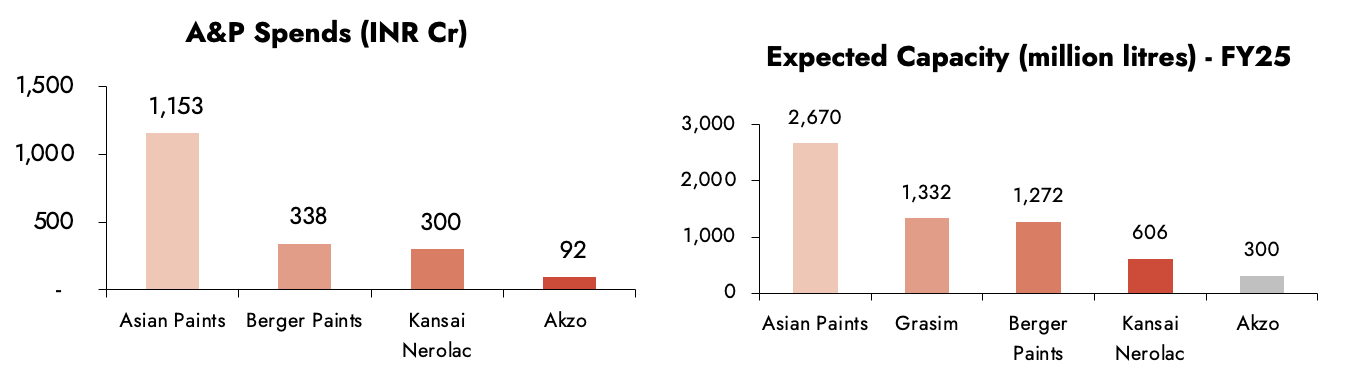

- Marketing and distribution are 2 important matrices in the paints segment – Asian Paints A&P spending is still substantially higher than all the other paint companies combined. Distribution of Asian Paints is unparalleled with dealers over 75000 and touchpoints over 1,50,000, with MBO’s being the bulk of sales for the sector, it will be extremely difficult to gain market share from Asian Paints. (Exhibit 4)

We acknowledge Grasim’s entry, capital employed and anticipated capacity coming on board however, we believe risks to earnings will be faced more by other larger players.

Exhibit 3 – Increase in Profit Market share for Asian Paints

Source: Ambit Asset Management, Company

Exhibit 4 – A&P Spends for Asian Paints is higher than the entire industry combined while Capacity is also ~2x of the nearest competitor

Source: Ambit Asset Management, Company Source: Ambit Asset Management, Company

DOUBTS OVER THE ABILITY TO SCALE UP ADJACENCIES

- There are doubts over Asian Paint's execution in non-core areas i.e. – Home improvement and other segments –

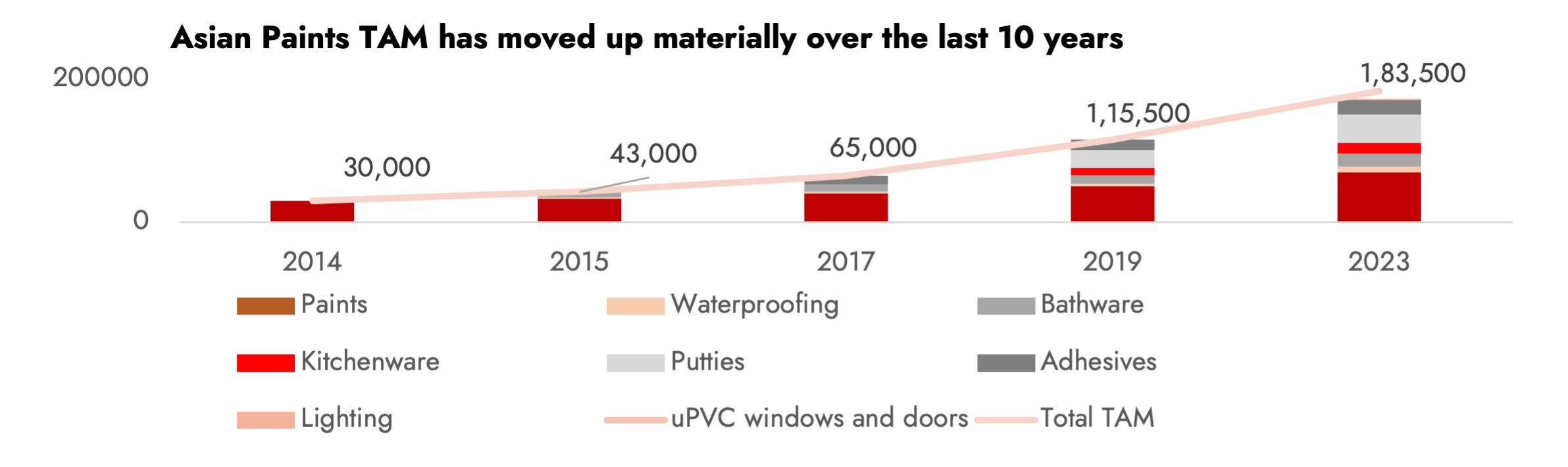

- However, the Estimated TAM for Asian Paints has expanded to closer to ~183,500 crores from ~30,000 crores a decade ago, with presence in newer segments having a TAM of <100,000 crores which is incrementally positive in our view. (Exhibit 5)

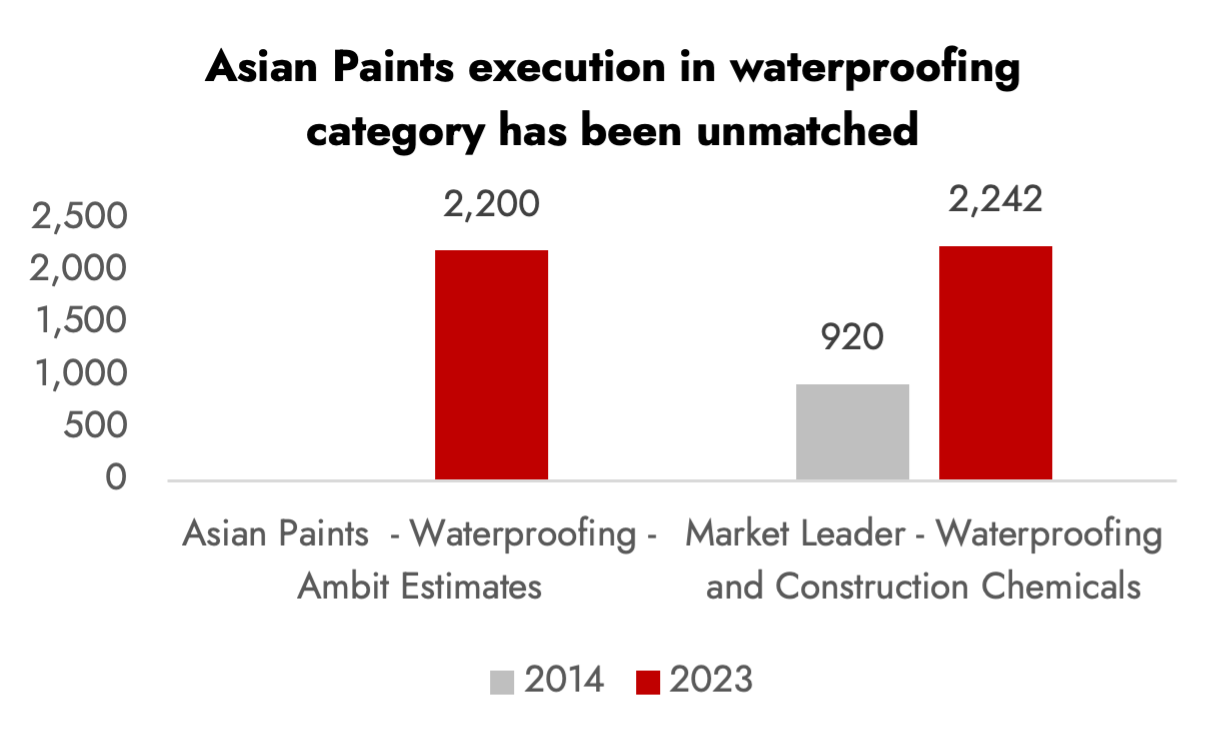

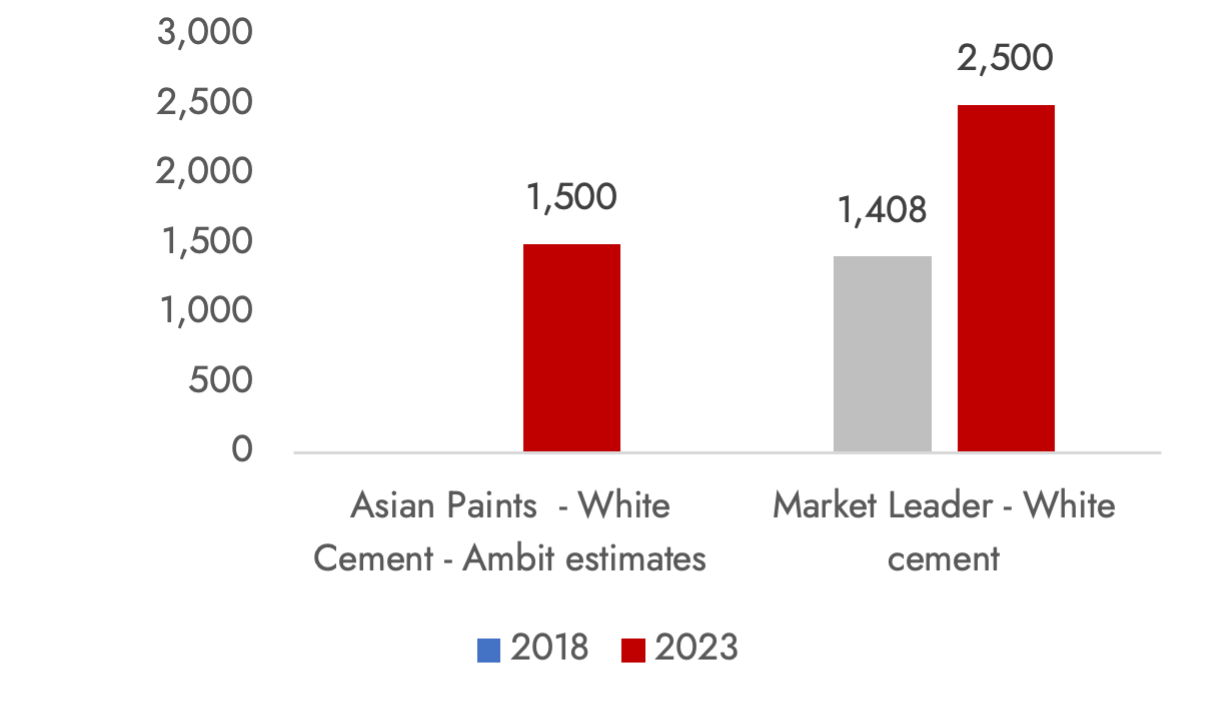

- Asian Paints' success in scaling up adjacencies in both waterproofing and white cement is proof of execution. (Exhibit 6)

- We anticipate similar success in growing categories and see Asian Paints as a home-building player in the future rather than a paints company.

Exhibit 5 – Increase TAM for Asian Paints

Source: Ambit Asset Management, Company, Industry sources.

Exhibit 6 – Asian Paints execution in water-proofing and White Cement has been unmatched

Source: Ambit Asset Management Estimates, Company. Numbers denote Revenue in crores

We anticipate seeing the full brunt of competition by Q1 FY25, and we anticipate Asian Paints to mitigate the competition and continue the growth trajectory post that. Near-term headwinds aside, we anticipate most fears of the market to be allayed by H1FY25 and the company to outperform in the next 12-18 months.

HDFC Bank:

HDFC Bank has moderated from peak valuations (4.24 P/B to 2.1x P/B) owing to the following concerns:

- The exit of CEO Aditya Puri and technical glitches resulted in RBI restrictions on new credit card customers, causing the beginning of a decline in HDFC Bank's premium valuation.

- Mega-merger: The merger with HDFC Ltd., has raised concerns over valuation due to potential ROE suppression from additional regulatory requirements of SLR, CRR, PSL, etc. on a merged entity and other technical reasons relating to outflows technical factors.

Peers catch-up: Most of the issues of growth, tech, and asset quality were addressed by both private peers and PSU Banks. Now competing strongly with the bank, unlike pre-covid times.

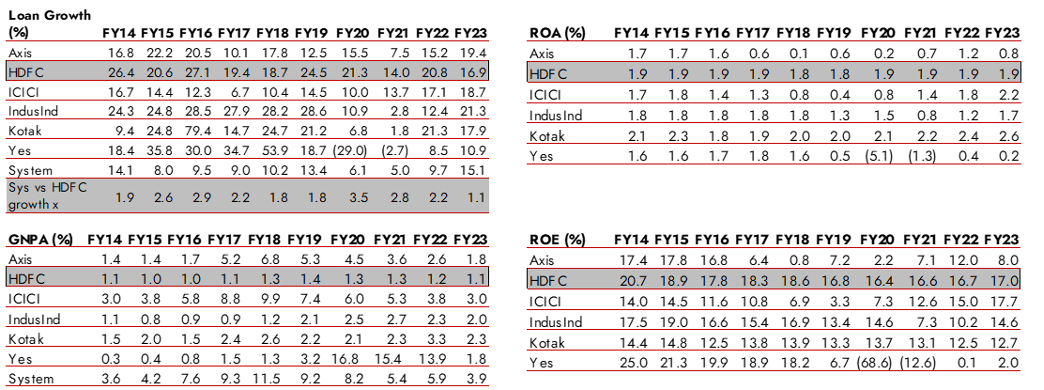

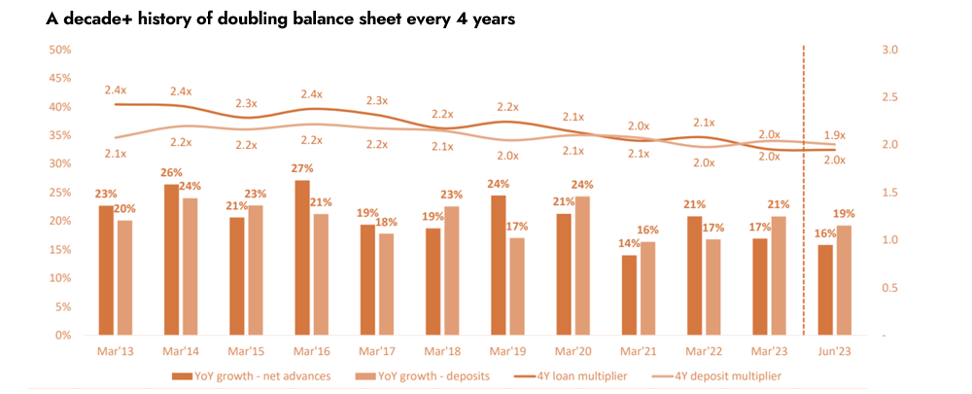

Exhibit 7 - HDFC Bank demonstrates solid loan growth, ROA, GNPA and ROE

Source: Ambit Asset Management, Company

- HDFC Bank has remained a leader and benchmark in terms of product innovation, growth and asset quality.

- Given the sharp run in small-size banks and PSU banks (now trading at above mean valuations), HDFC bank would become safe heaven once the flight to safety starts happening in other investment segments.

- Given ROE of 16-17% and growth of 17-19% (Exhibit 8), we see HDFC Bank as a fundamentally strong bank with limited potential of de-rating from current levels.

Exhibit 8 - HDFC Bank historical track record has been unparalleled

Source: Ambit Asset Management, Company

- HDFC Bank has the potential to re-rate, given its historical track record of strong ROE and higher growth and we anticipate HDFC Bank to outperform in the next 12-18 months.

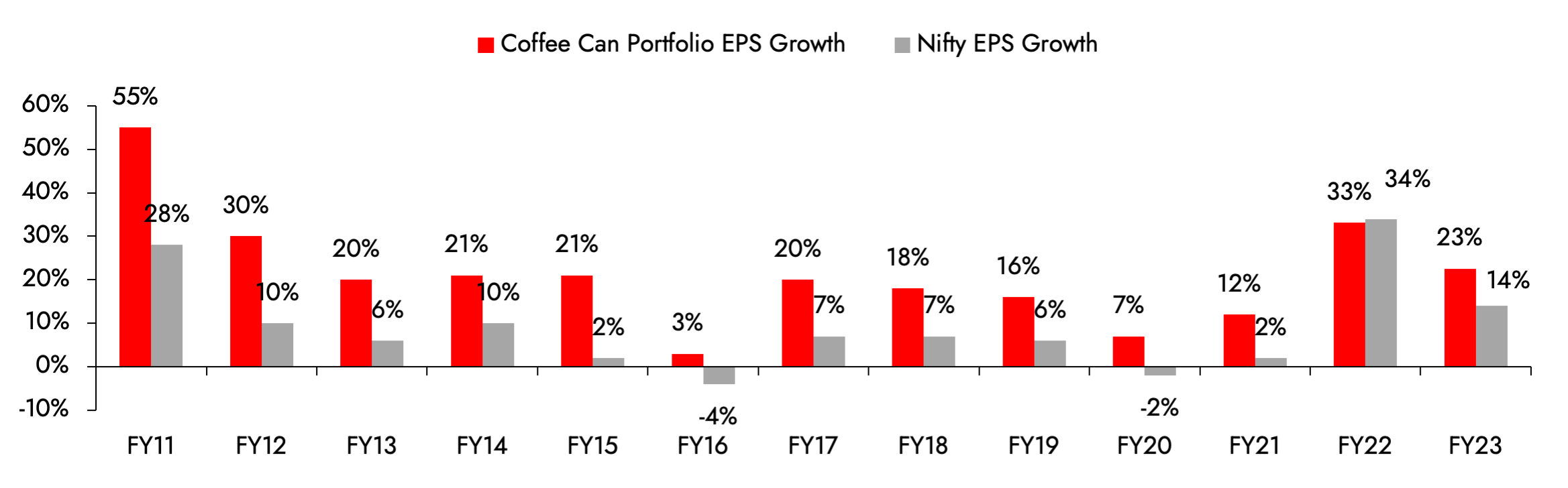

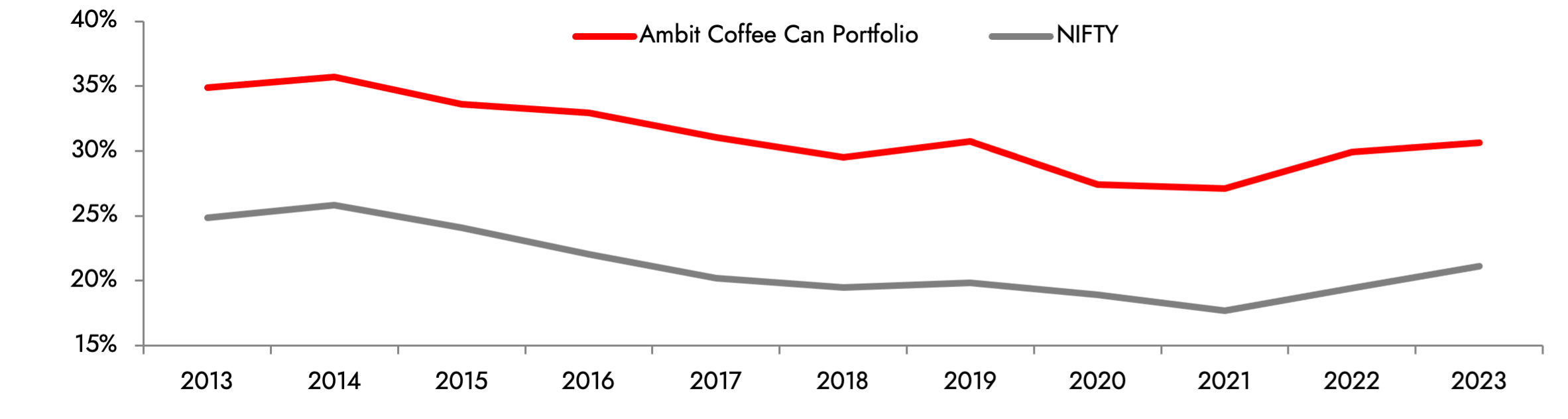

We anticipate the next leg of the rally to be fundamentally driven and companies who have not participated in the current rally despite strong operating performance (growth and ROCE) and are anticipated to deliver strong future earnings to be at the forefront of the same.

Exhibit 9 - Ambit Coffee Can Portfolio has both better growth and substantially better ROCE (800-1000 bps superior) resulting in consistent wealth creation.

Source: Ambit Asset Management, Bloomberg.

It’s not only the large caps where we see outperformance, we also see pockets in mid-caps and small-caps take the case of PI Industries and Garware Technical Fibres–

PI Industries valuation has moderated (from 53x to 34x) owing to concerns over sustainability of growth rate owing to -

1 – Increase in exposure to single-molecule

2 – Ability to scale up the pharma side of business

EXPOSURE TO SINGLE MOLECULE

- PI Industries works with all major global ag-chem innovators, however, a large portion of PI’s growth has come from working with Japanese innovator – Kumiai Chemicals, particularly the product Pyroxasulfone.

- Pyroxasulfone has grown at ~29% CAGR over the last 5 years. We anticipate the growth owing to better penetration in existing geographies (US and LATAM), an increase in the number of geographies and an increase in applicable crops.

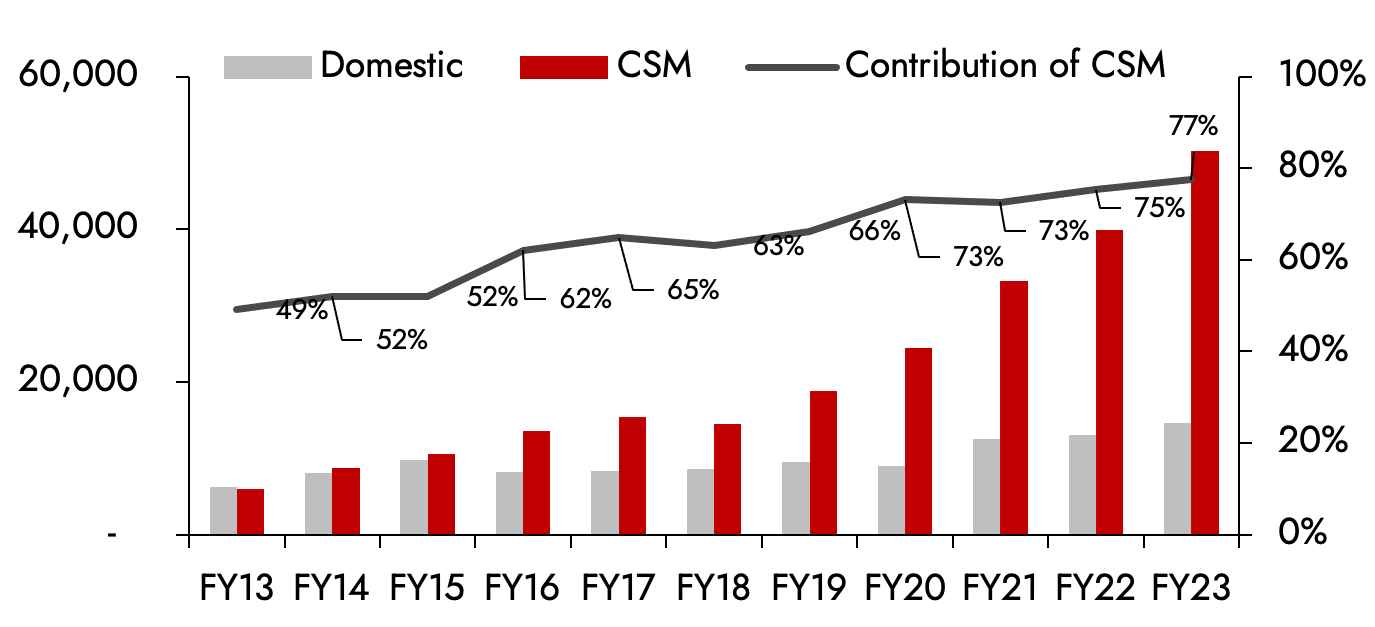

- PI has effectively grown CSM and now contributes over 77% to overall revenues de-risking the domestic portfolio and showcasing PI’s diversification and execution skills. (Exhibit 10)

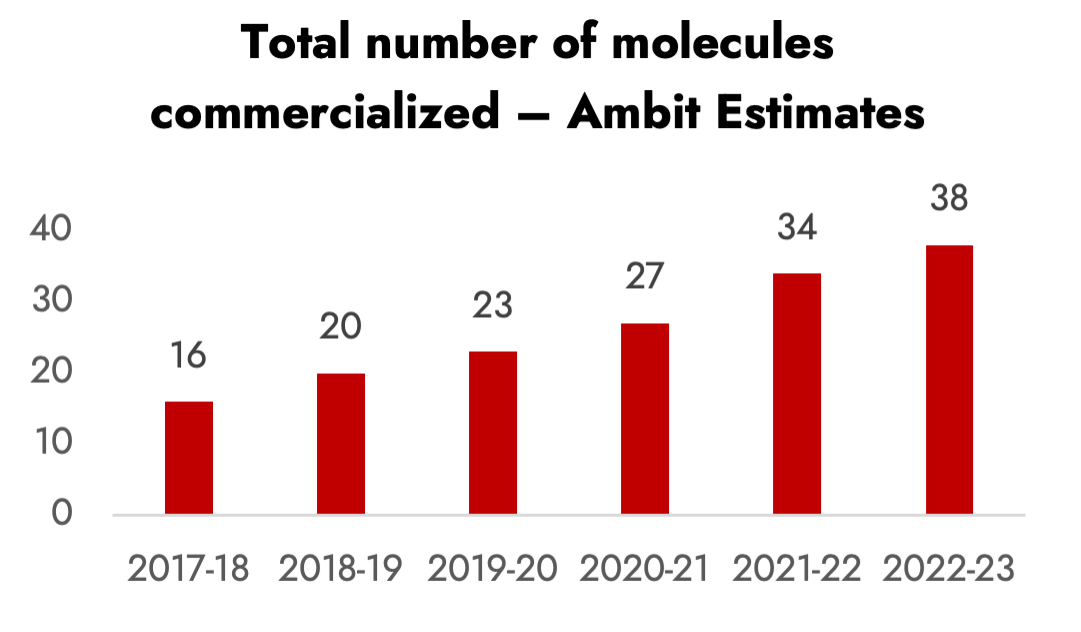

- Over and above, PI Industries has increased the number of molecules commercialized to ~38 from around ~16 in the last 5 years. We expect the increase in commercialization to reduce single-product risk and anticipate the growth trajectory of PI Industries to continue. (Exhibit 11)

Exhibit 10 – CSM growth has grown at a CAGR of 24% over the past decade

Source: Ambit Asset Management, Company. (Denotes Revenue in million)

Exhibit 11 – Number of molecules commercialized has increased materially over the last 5 years

Source: Ambit Asset Management, Company

ABILITY TO SCALE UP PHARMA BUSINESS

- PI Industries raised ~2000 crores in 2020 primarily for inorganic acquisitions in the pharma space. In May 2023, PI announced acquisitions of ~900 crores for Archimica and TRM which have a presence in CRDMO and API’s. In addition to the same, PI has surplus cash of ~2900 crores as of Q1 FY 24 which can further accelerate the pharma push

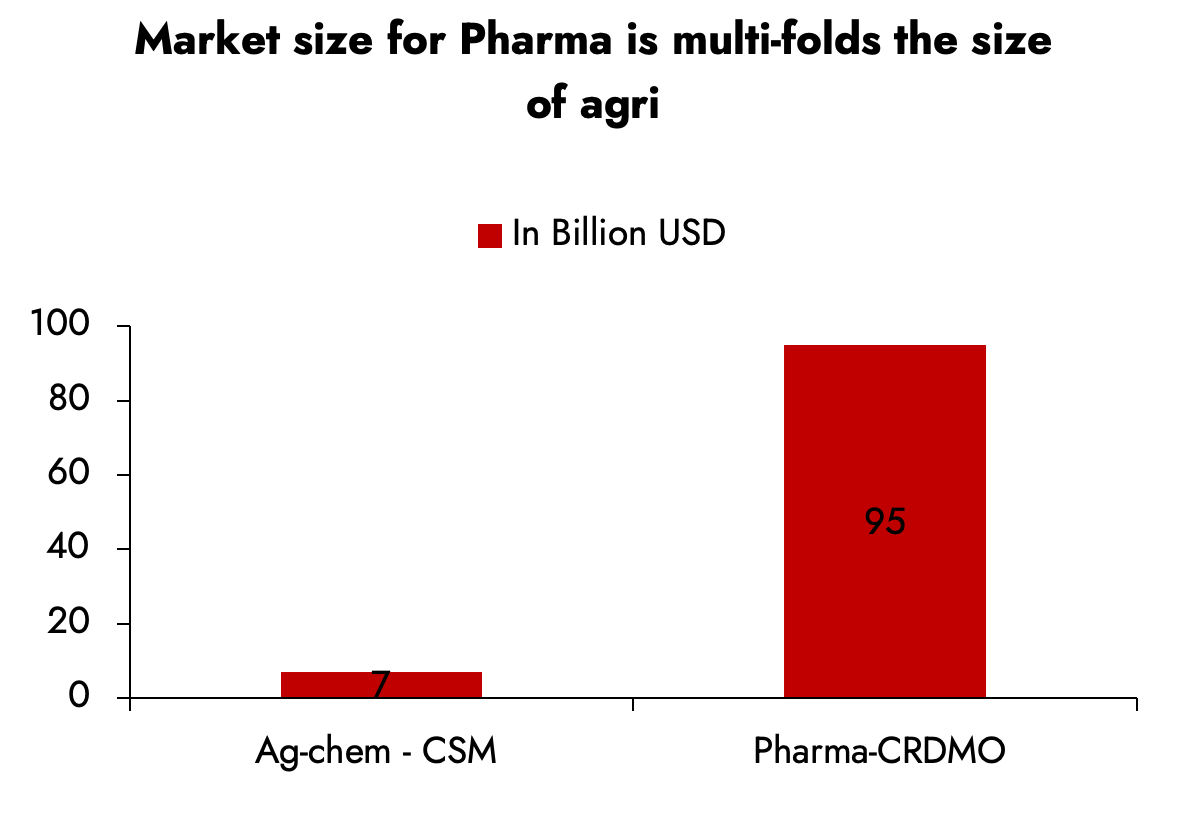

- Pharma market size opportunity is multi-folds the size of agri-opportunity. (Exhibit 12)

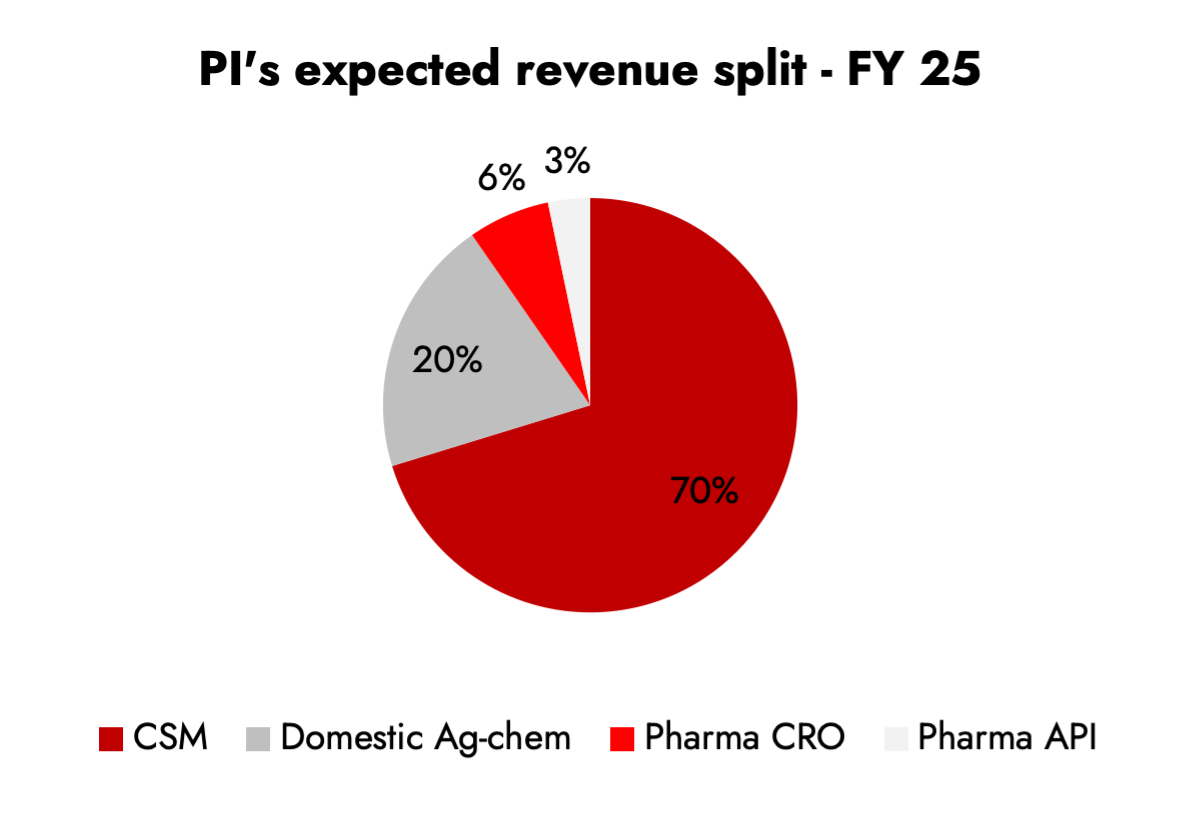

- We believe PI is well set to replicate success in Ag-chem CSM to pharma- CRDMO owing to both organic initiatives and inorganic acquisitions and historical track record. (Exhibit 13)

Exhibit 12 – Market size for Pharma CRDMO is >10x the size of Agri-CSM

Source: Ambit Asset Management Estimates, Company Media sources, Syngene AR

Exhibit 13 – Pharma is anticipated to be atleast 10% of revenue by FY 25

Source: Ambit Asset Management Estimates, Company

We anticipate PI Industries to continue delivering industry leading growth owing to strong execution, and an increase in opportunity size and expect fears of the market to be allayed by Q1 FY25 and anticipate strong performance in 12-18 months.

Garware Technical Fibres valuations have moderated from – (45 x to 27 x) owing to:

- Risks to growth profile due to challenges in aqua-culture and sports segments.

- We have written a detailed note on GTFL in March 2023 – ( https://www.ambit.co/public/Ambit_Disruption_VOL20_GARWARE.pdf)

- The aquaculture segment which is the most profitable business for Garware Technical Fibres was facing uncertainty due to the proposed Resource rent tax which was finalized at 25% v/s 40% earlier.

- With the resource rent tax now out of the way, we note the growth in aquaculture remains strong due to the focus on innovation by GTFL. In the past few years, innovations such as Sapphire X18 and V2 have helped Garware mop up substantial market share in key geographies in Norway and Chile.

- Sports segment which has been a key growth driver for Garware Technical Fibres over the past few years faced several challenges due to over-stocking. We anticipate the challenges faced last year will ease off in the coming quarters and the sports segment to be a key growth driver going forward for GTFL.

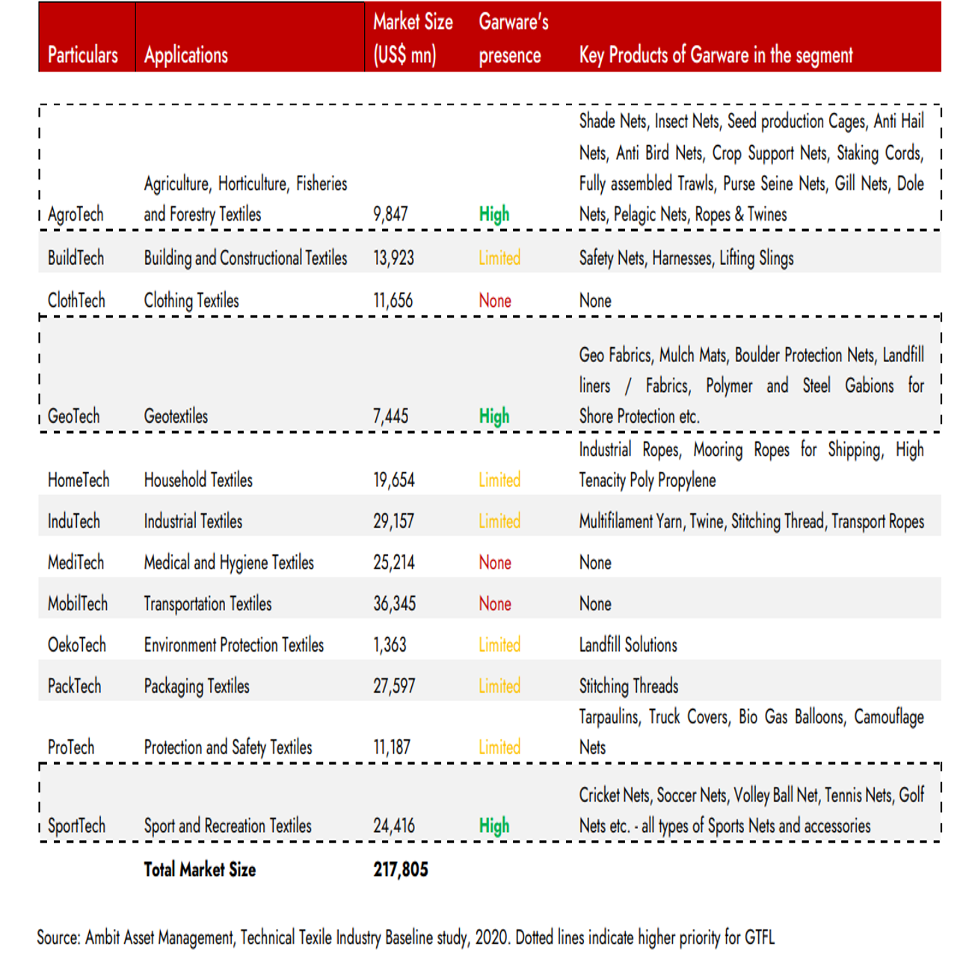

Geo-synthetics which was a very small part of total revenues a few years back has shown remarkable growth and adds another lever of growth for Garware. Notably, the return on capital employed in Geo-synthetics is the highest in GTFL’s portfolio which should enhance Garware’s already impressive ~47.2% ROIC.

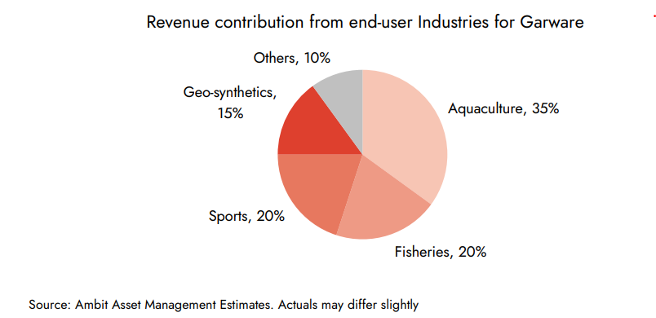

Exhibit 14 – Revenue contribution from end-user industries for GTFL

Exhibit 15 – Addressable Market size for GTFL is huge

- With ~70% of total businesses in an accelerating growth phase, we expect Garware to deliver industry-leading returns over the next 12-18 months.

CONCLUSION

Small > Mid > Large Caps has been the theme over the past 9 months primarily driven by liquidity. We anticipate the next leg of the rally to be driven by fundamentals and earnings growth will be at the forefront. In addition to earnings, valuations have moderated especially amongst large caps and pockets within small and mid-caps which should lead to strong stock performance in the future.

Our portfolio companies across all segments Large, Mid and Small Cap are well poised to deliver industry-leading earnings growth and we anticipate the same to translate into benchmark outperformance in the near to medium term.

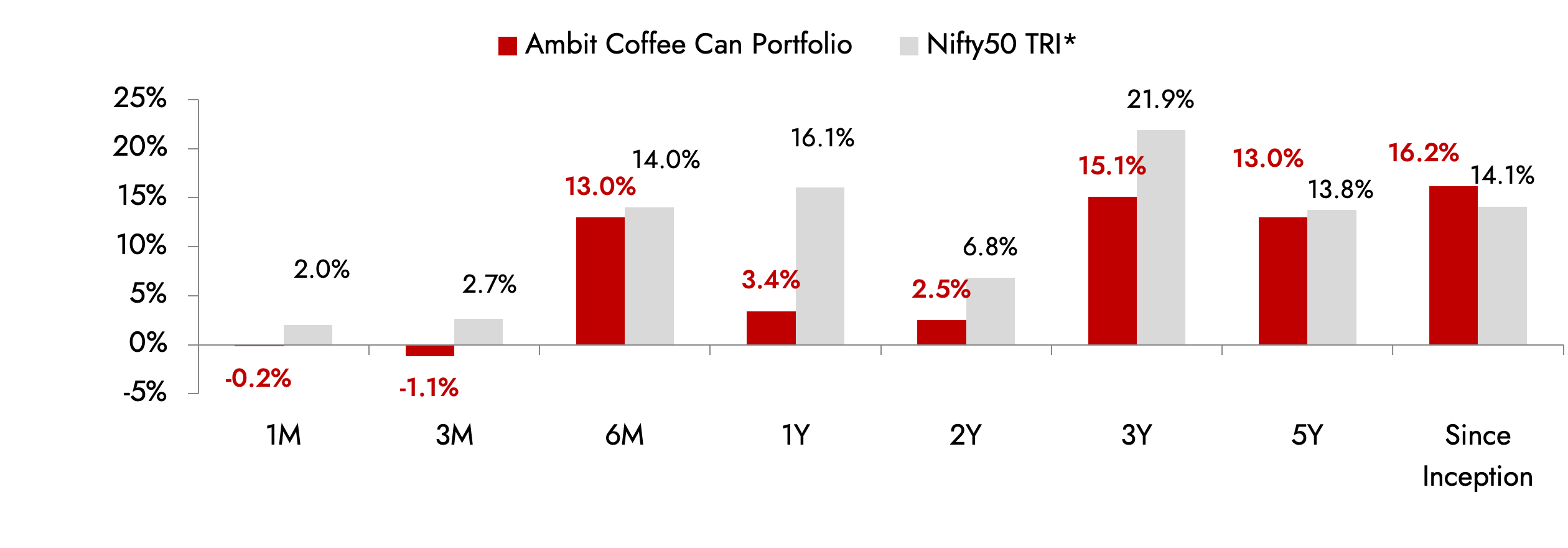

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 16: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of May 31st 2023; All returns are post fees and expenses; Returns above 1 year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts. * Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

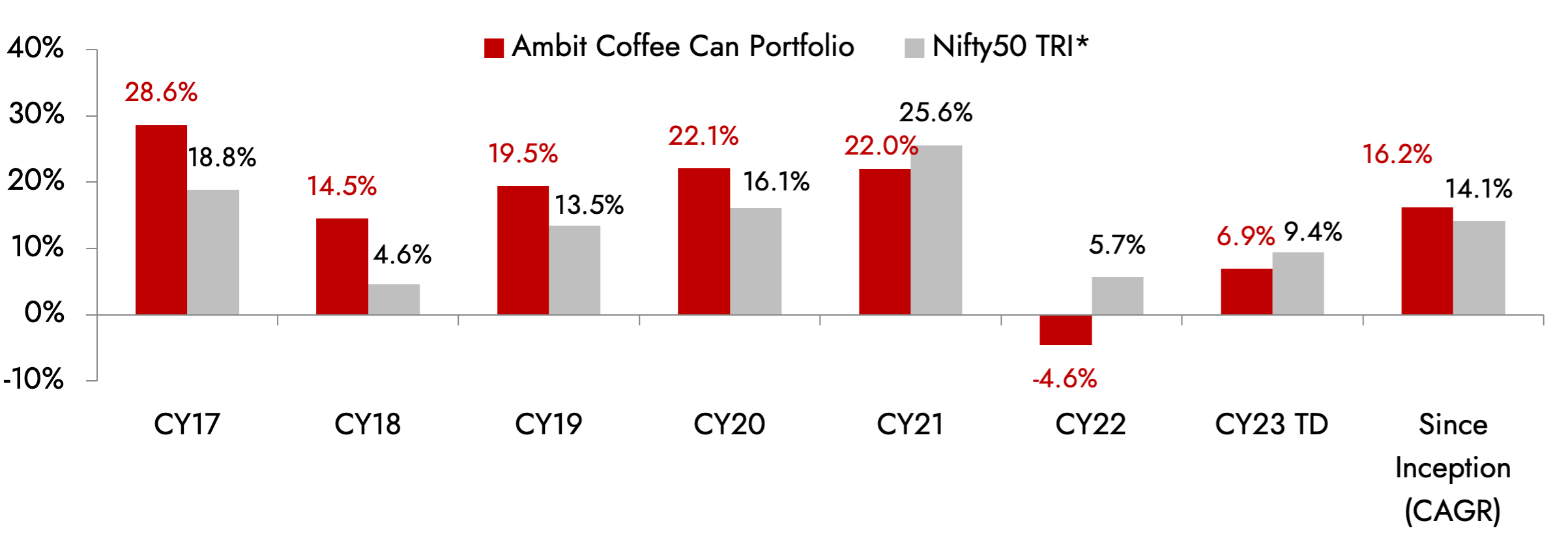

Exhibit 17: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of May 31st 2023; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts. * Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

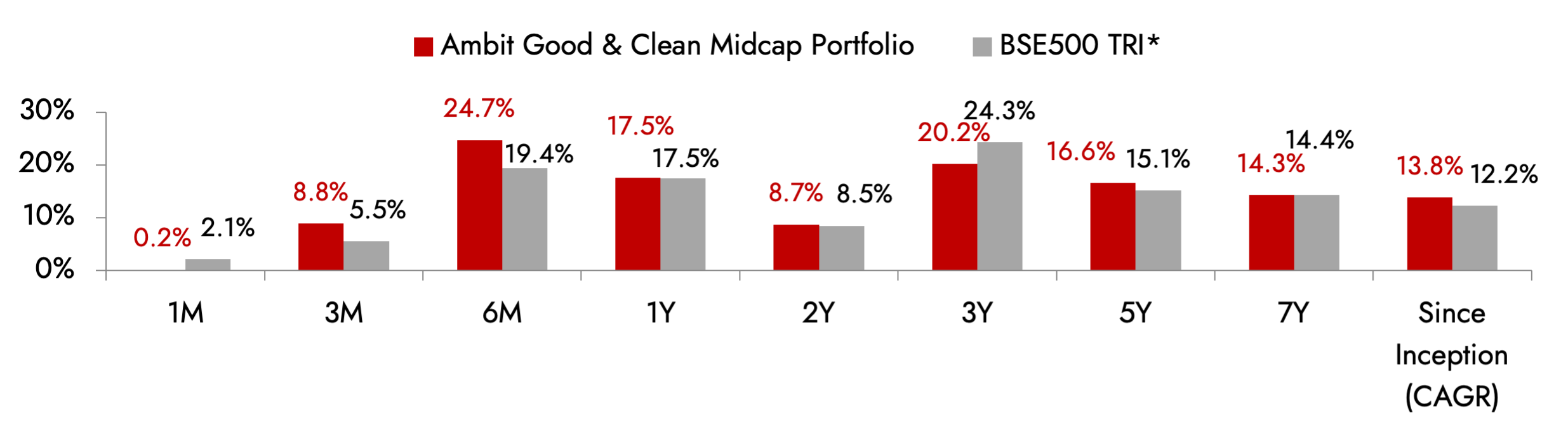

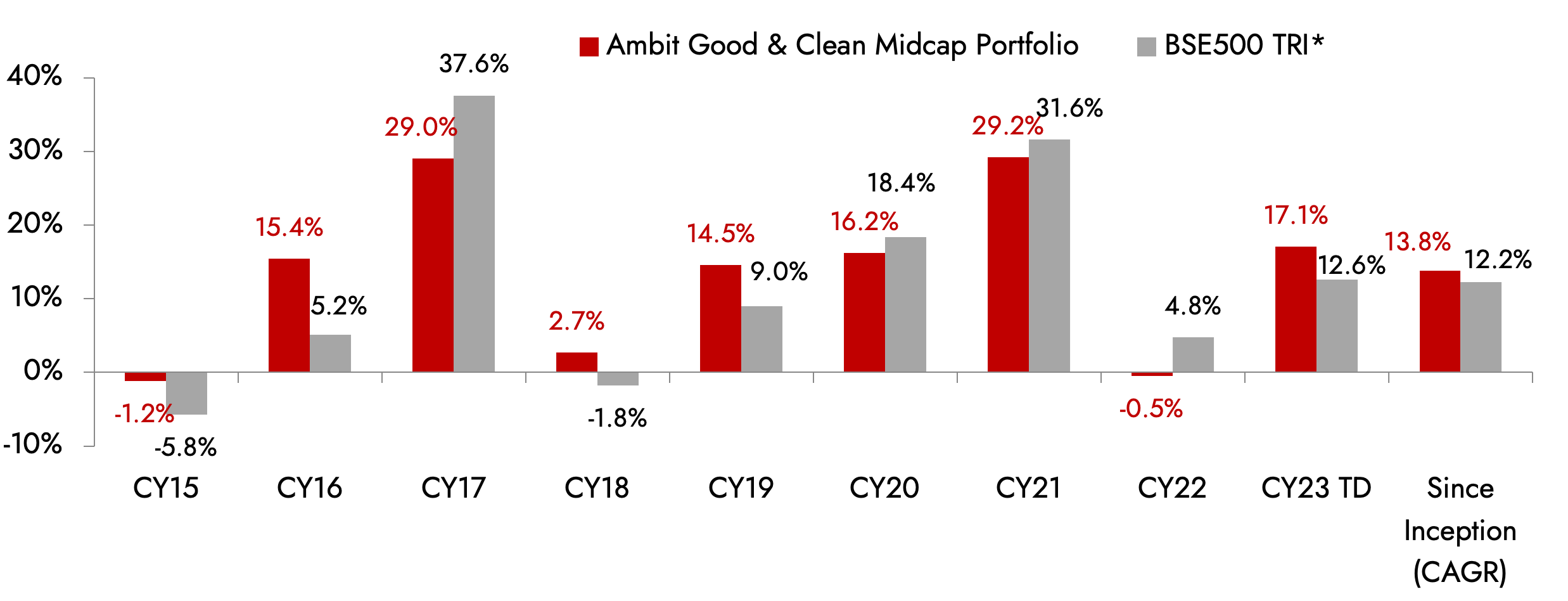

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 18: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of May 31st 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI.

Exhibit 19: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of May 31st 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI.

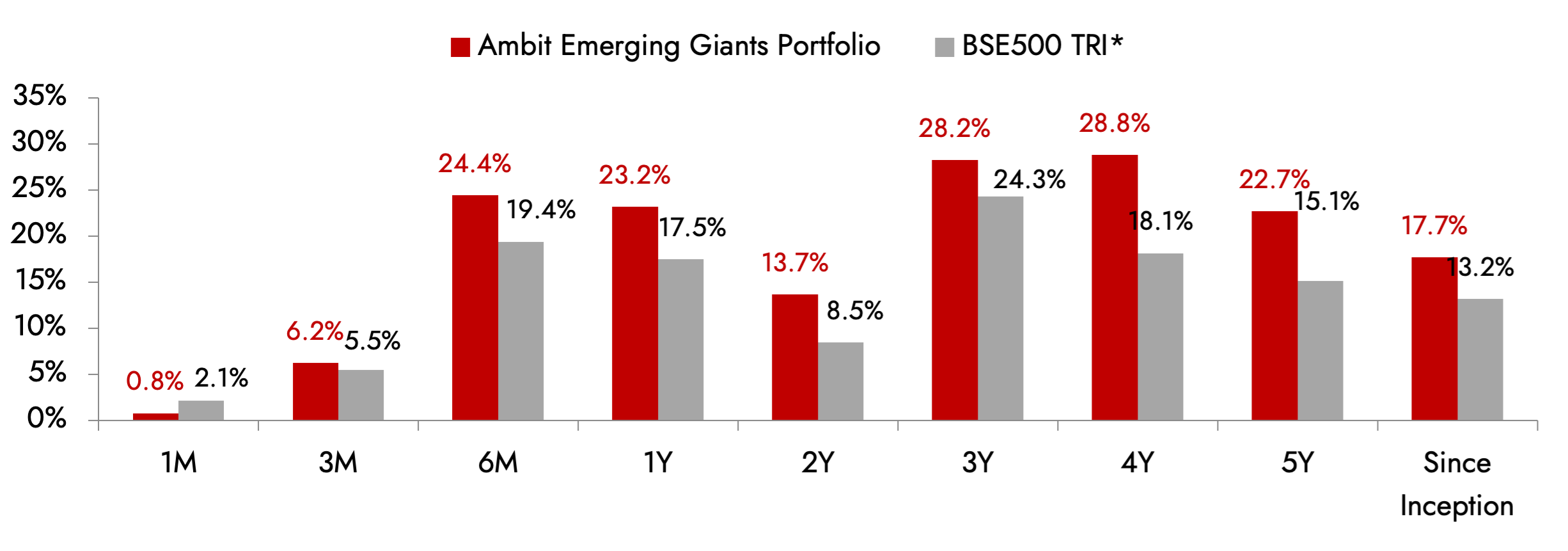

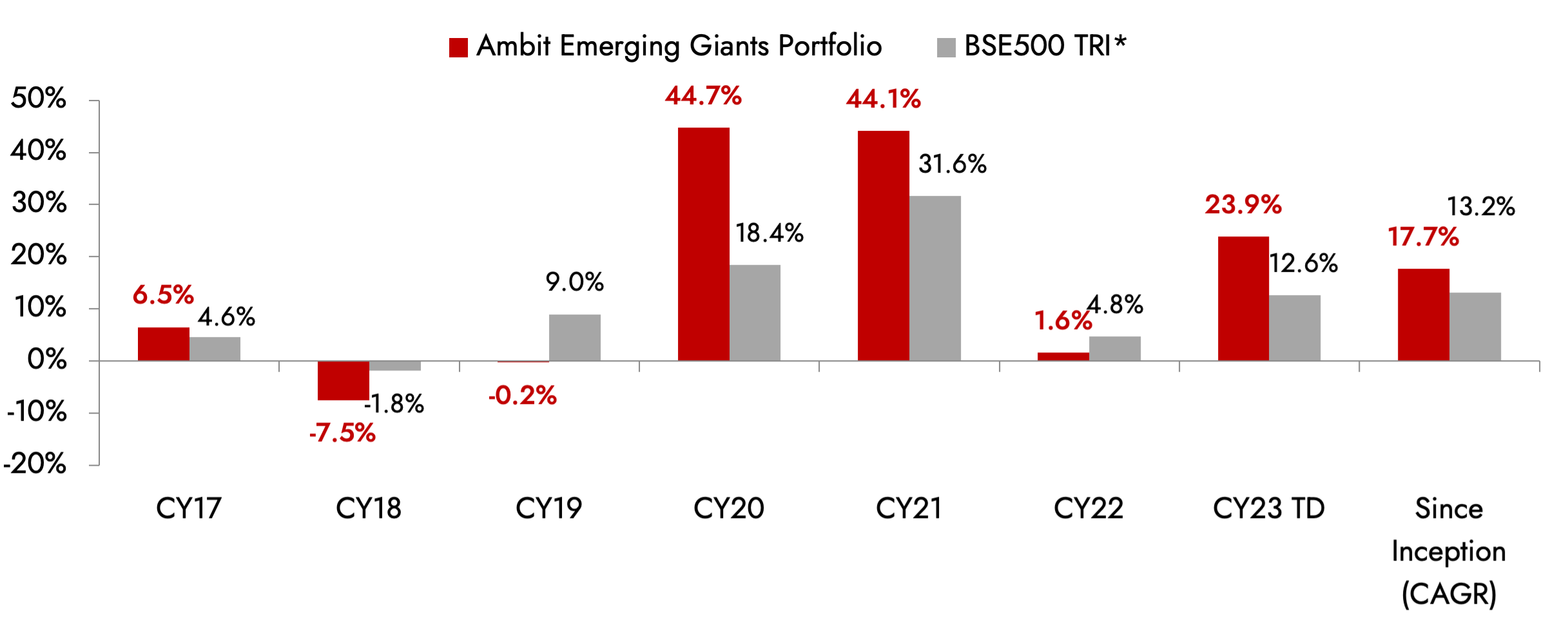

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 20: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of May 31st 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI.

Exhibit 21: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of May 31st 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI

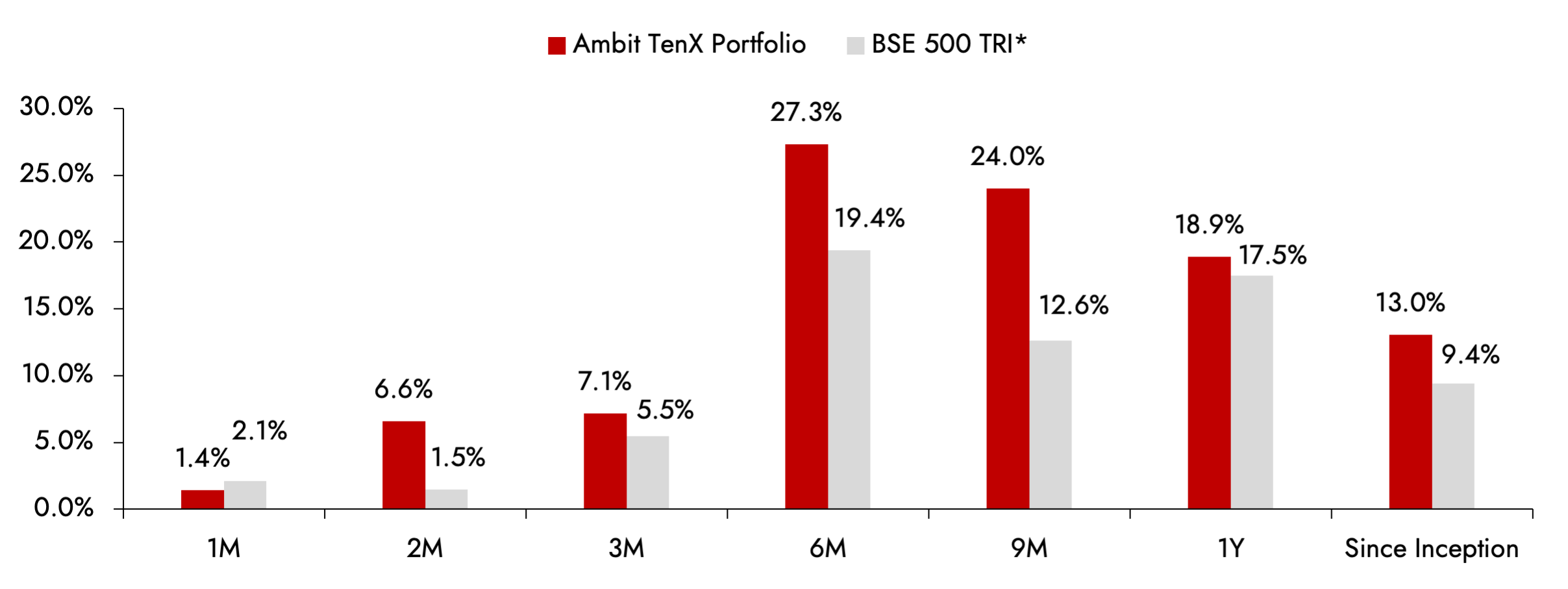

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follows:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 22: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of May 31st 2023; Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

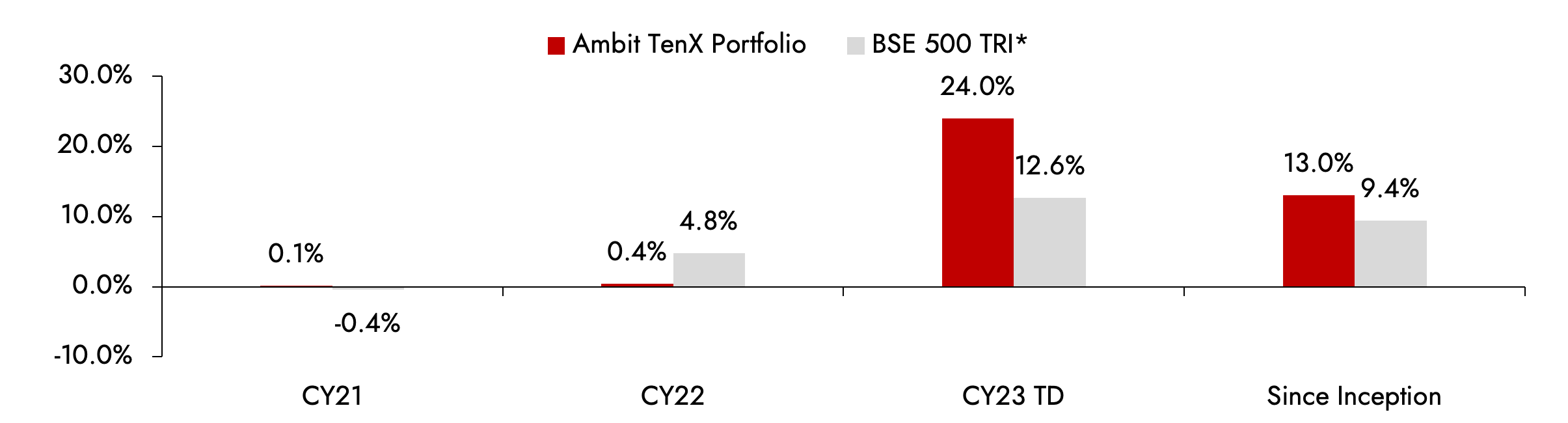

Exhibit 23: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of May 31st 2023. Returns are net of all fees and expenses. *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

For any queries, please contact:

Umang Shah - Phone: +91 22 6623 3281, Email - [email protected]

Registered Address: Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Corporate Address: Ambit Investment Advisors Private Limited - 2103/2104, 21st Floor, One Lodha Place, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein. Returns are calculated using TWRR method as prescribed under the revised SEBI (Portfolio Managers) Regulations, 2020. Performance is net of all fees and expenses. Past performance is not a reliable indicator of future results. Please note that performance of your portfolio may vary from that of other investors and that generated by the Investment Approach across all investors because of 1) the timing of inflows and outflows of funds; and 2) differences in the portfolio composition because of restrictions and other constraints. For comparative Performance relative to other Portfolio Managers within the selected Strategy, please visit: bit.ly/APMI_PMS

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/ graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020

You may contact your Relationship Manager for any queries.